Live Music Archive

Live Music Archive Librivox Free Audio

Librivox Free Audio Metropolitan Museum

Metropolitan Museum Cleveland Museum of Art

Cleveland Museum of Art Internet Arcade

Internet Arcade Console Living Room

Console Living Room Books to Borrow

Books to Borrow Open Library

Open Library TV News

TV News Understanding 9/11

Understanding 9/11tv U.S. Senate CSPAN February 8, 2013 9:00am-12:00pm EST

9:00 am

i'm not just defending strasbourg because it's in the treaty. i defend strasbourg because its history that seeks the role that strasbourg house to play. we celebrate the 50th anniversary of the treaty of friendship between germany and france elite, and strasbourg was part of that reconciliation between our two countries. strasbourg is both a history in the future of germany. it's the city that represents what europe is. i'm not just defending it because it's in france. europe has other seats in other countries. i defend strasbourg, strasbourg in europe. if you think that it shouldn't be the seat of the european parliament, then doubts undermines everybody's view of europe. so thank you very much for having me here in strasbourg at

9:01 am

the seat of the european parliament. [applause] [speaking french] >> translator: thank you, mr. president. >> you were watching c-span2 with politics and public affairs. weekdays feature live coverage of the u.s. senate. on nights watched key public policy this. and every week in the latest nonfiction authors and books on booktv.

9:02 am

you can see past programs and get our schedules at our website, and you can join in the conversation on social media sites. >> the programs that we had all under -- >> we are live now as u.s. chamber of commerce is hosting a quarterly briefing today on the outlook for the u.s. economy. martin regalia, chambers chief economist will talk about recent gross domestic product figure and what policy the obama administration and congress to propose to help stimulate the economy. this is just getting under way. >> a prime example of our ability to involve experts and debates on topics that are critical to the business community. i'm going to start us off today by queuing a video from christopher giancarlo of the gfi group, our sponsor, for this series. but for some want to make a brief announcement. this series, this economic series that we pose every quarter, has been accredited by the national association of state boards of accountancy to

9:03 am

provide continuing professional education, credits for accounting professional. so we are quite excited of that and hopefully you will as well. this accreditation highlights the value of this and other programs that would hold her at the chamber. for more information on that please visit our website, or speak to some of folks outside in the registration desk. after the video i'm going to ask marty to come up directly and begin the program the first award from our sponsor, the gfi group. >> good morning. gfi group is delighted to continue its support of the national chamber foundation's quarterly economic briefing. the goal is to affect the impact of public policy on u.s. bases and the global economy. gfi group is an american company headquartered in new york city with shares trade on the new stock exchange. gfi employs close to 2000 people and over a dozen offices and most of the world's major

9:04 am

financial centers. as you meet us when gfi employs are hard at work around the globe and here in new york and executing billions of dollars in transactions across a range of foreign exchange, interest rates, treasury, credit, equity, commodity and energy. gfi group is a wholesale broker come sometimes called an interdealer broker. the rest of the industry go back over a century in the world's major financial centers. gfi has institutional clients in transacting exchange listed products and also operates exchanges for things that don't trade on traditional exchanges, instruments that are instead traded over-the-counter such as swaps and other derivative instruments. 15 months ago congress passed the dodd-frank act including title vii that requires when possible that stock transactions be cleared, reported and execute on exchanges, or swap execution

9:05 am

facilities. congress recognized global swap workers won't be widely served by firms such as the gfi group. it was great to reflecting on standing role and recognize terms like gfi into the nod the new dodd-frank regulatory framework. the fec and the cftc are still at work on detailed regulations. that will impact the entire process of trading swap in the united states and abroad. getting those rules right now impact not just the large banks and swap dealers that make markets. but also the american businesses that use swaps to lessen the vouchers to better manage capital for growth and investment in u.s. jobs. those rules will reflect the effect not just wall street, but economic conditions on main street. gfi group stands for a swaps regular regime that improved

9:06 am

registry transparency, promotes competition and increases market participant access. gfi has been vocal in support of the clearing, execution, and reporting mandate of dodd-frank, through dozens of public writings and formal congressional and regulatory testimony. through decades of experience in the financial markets leads to concerned that some currently propose sec and see sec rules are overly prescriptive, may harm market liquidity, increase trading costs, and worse, may drive trading in some swaps products offshore. this result would negatively impact the u.s. capital formation and the u.s. businesses and jobs that depend on. instead, market regulators should probably implement the see reform of the dodd-frank act, central clearing, regulated execution, and enhanced transparency. without overreach and

9:07 am

complication. they must turn away from attempt to reengineer swaps markets with a series of one size fits all rule. and instead, turn to flexible, principle face approach that reflects the importance of these markets of u.s. economic recovery. it is time to get on with the work of putting u.s. swaps markets on a sounder footing with greater transparency, for proper financial risk management, allowing investing back to prosperity. gfi group is places for the national foundation in ensuring that all public policy, whether related to use swaps markets or in any other way related to u.s. business activity, is one examined for its impact on u.s. economic growth, market vibrancy, most critically, u.s. job creation. thank you for your time this morning. it's my pleasure to introduce the use chambers chief

9:08 am

economist, dr. martin regalia. thank you. [applause] >> well, thank you all very much for coming out on such a rainy day. to listen to economists. we will live up to our reputation as dismal scientist this morning i think. i'm pleased to have three very distinguished economists this morning to help me kind of sort through some of the economics, anderson's idea a little bit of five to 10 minute presentation, then each one of them are going to speak of and then we will sit down and can't have a discussion, open it up to questions from the audience. today we have john felmy, chief economist at api and who will talk to us about kind of energy. john won't do forecasting energy prices, but he will talk about the energy situation is looking and what we are seeing in terms of more exploration energies,

9:09 am

supplies, a huge sector in the us economy and one of has made a focal point of our growth strategy going forward. so it will be very interesting to hear from john. will also hear from frank nothaft was a chief economist at freddie mac, and frank is an expert. i've known frank for -- i was held on, because he looks much younger than i do, but it's a long, long, long time, and he is an expert in the housing market and i think that's one of, if not bright spots at least brighter spots in the economy today. and then finally we'll have bob costello was the chief economist at ata. in this economy we build stuff that would put on trucks and we move it around. so if you're trying to keep track of the trucks you can also keep track of the economy and bob does an amazing job of that. i'm happy they all agree to be here this morning. when you look at the u.s. economy today we see an economy that have started growing three and half years ago. the problem is that it never hit its stride.

9:10 am

it grew but it grew at an average of about 2.3% which is virtually our long run potential. and as a result we never made up the gdp gap from what was a very steep and prolonged economic downturn. so you've seen this chart in the recent cbo, a little different because cbo has that line kind of turning up and catching the red line at some point in the not-too-distant future, and i don't and that's because i'm not that optimistic. that we are going to see growth in excess of 4% as cbo has forecast. and without that, you don't close the gap. this is what really is the problem in the u.s. economy. we have grown. we are doing better than we were four years ago. we are above the blue line is above what it was four years ago when we were in the depths of the reception. -- recession. we are not really doing anything to get it back where it was. in fact, if you look at the last

9:11 am

three or four economic recoveries, you see that the ones prior to 1991 had the shakes. they fell off sharply and then they came roaring back as real we put people back to work for quickly. this one as the prior to, but even more so, kind of meanders along when they started back a. so we never really charged back with four, five, six, seven, eight, nine, 10% growth in real terms. we kind of wobbled along at three, then at two and a half, this time around at 2.3. that's the problem. and until we figure out why that is and what we can do to get the growth of backup, we are not going to close the gap. we're not going to get back and we will not put people back to work. we're still a million and a half or so short of where we were prior to the recession. the unemployment rate has held up in incredibly high. 7.9%, and that's only the only reason it's that low is because

9:12 am

the participation rate has dropped to a 30 year low. we have participation rates that we haven't seen since women started entering the workforce. 38, 39%, 37% of americans of working age don't participate in the economy. that is a damning statistic that doesn't seem to make it in to the front pages. and if we don't see any continued drops in the participation rate, which would be truly unprecedented, we're not going to see continued improvement in the unemployment rate. last month, 150,000 jobs, little bit worse than 180,000 average the year before, unemployment rate ticked up one-tenth of 1%. i really appreciate the euphemistic approach taken by bof when the parade was taking than one-tenth of 1% it was unemployment rate drops. this time it was unemployment rate remained virtually the

9:13 am

same. one-tenth down to one-tenth of kuroki can we are not making headway. that's the bottom line. and in order to make headway you have to get our growth rate a. it's not all bad news. because of this year we are starting to see finally some of the underpinnings, real cite underpinnings of the economy look better. the things that look the same our kind of self-inflicted wounds that our political process keeps tossing on the economy. so as you look at the housing market is getting better. frank will talk about that today. it's important and it's not just important because of jobs and because the more buildings and housing construction. it's important because the prices are starting to come back and that means the underlying value of the homes and the net worth of the average american is starting to come back from at that net worth will help drive consumption. we are seeing the fed continued a very aggressive policy.

9:14 am

very aggressive and they've given us some metrics to watch for, 6.5% on upon, to% and inflation. we don't see either of those in the forecast of future the next year, year and have so we think the fed will remain fairly aggressive. that's going to be a big plus for the economy. we see europe, it's kind of off the headline, and from europe no news is good news. so what we are seeing is no more talk about the euro exploding. we're seeing the euro strengthening of it. not really great for european growth, but not bad for hours. and we are also starting to see them kind of kick the can down the road on their debt problems, so they're not propping up with three-month regularities so it's a quarterly crisis. things have settled out a bit there. they're going a little bit better and there started to come out of the recession may have been in now for about nine months. and that's all positive. so those things look better. the whole energy sector is booming in this country, and that's a plus. and as a result, my forecast,

9:15 am

not john's, for energy prices is that we're not going to see the kind of, you know, early summer, late summer driving season spikes that are played economy in the past. able to lift up a bit from where they are now, but i don't see the kind of spiking that we saw in prior quarters, prior summer months. and that's a plus. so all of these things factor in. in addition, businesses both here in the united states and abroad have huge cash and none of these business go into business to hold cash. the problem is that the uncertainty out there, and the fact that the economy hasn't picked up so the capacity utilization in this country at about 70%, is low by historical standards. there's excess capacity even today. and so there's not the exigency to invest that has existed in prior economic upturn. we think that that cash is going

9:16 am

to start filtering back into the economy and, therefore, investment perhaps the second most important factor in economic growth will start to pick up a bit as the year goes on but it's going to be gradually, improvement will be gradual. and on the downside we have thrown a lot of roadblocks in its path. we have a debt and deficit situation which in the long term are unsustainable, and we're doing absolutely nothing to correct that. nothing. i know cbo's forecast was that we would see modest improvement in the jet crashing into debt-to-gdp ratio the next two years but i don't believe the. i don't like their forecast. i do with 4% growth is going to venture lies with the 0% increase in the interest rate. just don't see it happening. if you get when you're going to get the other one taking up and that will be very, very difficult to maintain a stable or declining debt-to-gdp ratio. but even cbo has a debt-to-gdp ratio picking up at the end of the 10 year horizon. so we have to stabilize the debt.

9:17 am

we haven't fixed the debt. and, in fact, we spread the crisis out so that we really won't go a month without one. we have the fiscal cliff at the end of the year. nothing was done in the later part of the year. and then in the 11th hour, actually it wasn't the 11th hour. it was about the 15th hour, two and half hours after we went off the cliff of the house hold us back on and in the senate a day later. but what do they do? they raised taxes, didn't cut spending, and essentially postponed some of the other issues, like the debt ceiling, which was going to come up very quickly in the new year, and now has been postponed to may 19. we also have a sequestration but was postponed for two months and that's coming back at the end of february. and if that wasn't enough we have a c.r., since we don't pass budgeting now, we governed by c.r. we have a continuing resolution debate and vote coming up on or before the 27th of march. so what we have done is we've

9:18 am

spread these crises out over the course of the whole first half of the year and that's going to be difficult for the economy to manipulate, because as we start istartto see fundamental improvt elsewhere, we will see continued refocusing on the inability of our government to come to terms with its spending, it's taxes, and its debt and deficit. and that will continually, i believe, while markets and call into question some of the more optimistioptimisti c factors that we are seeing. i'd like to call the panel up here, and we will start going through with we're going to do john first, and then we're going -- excuse me, we'll be frank first on the housing and then we will do jon and then we'll dupont, and will keep everything on schedule and we're trying to get you right out at 10:30. thank you. [applause]

9:19 am

>> thank you, marty. and i want to thank the u.s. chamber of commerce foundation for hosting the event here today, inviting me to participate. certainly my pleasure to be here. i have some slides i will refer to. in terms of the overall housing market, this is the most upbeat i have felt in years. we've had nothing but completely terrible news on the housing side for some time. we are starting 2013 to with a fair amount of inertia in the housing market. as you know over the past year, home sales are a. in fact, home sales are up about 9% compared to 2011, 2012 over 20 housing starts up about 25%, and house price indices have turned around. they all bottom out in 2012 and we've had some very good positive inertia on the housing side. and that i believe will continue into 2013. what i'll touch on today is a little bit on what's happening, what's really driving the housing market right now, what's driving housing demand, and i think a lot of it is based on

9:20 am

very low mortgage rates that helped to drive a ford built in the market place. i'll talk a bit about that. secondly, i will talk about some of the trends we've seen. house prices in natural indices are up five to 6% over the last year. i think we'll see another three to 4% increase in national house pricing in 2013. finally, i will share some thoughts on what we see for the mortgage market in 2013. let's first start with housing demand. as i mentioned we seeing a pickup in sales and new construction activity. i think in part this is driven by the high degree of affordability we see in the marketplace. and a very simple but straightforward metric of this is the national association of realtors affordability index. ipod that you on this target we intend to make it out. to hide the affordability index, these it is for typical come to afford to buy a home. the national association of realtors when they produced their a portable index the

9:21 am

incorporate three key ingredients that drive affordability for the prospective home buyer. those three ingredient our mortgage rates, house prices, family and can. mortgage rates, house prices and family income. and i plotted with those increase, the mortgage rates on the blucher. mortgage rates are at incredibly low levels. we are 33 year fixed rates at 3.5%, the lowest in at least 65 years. between that and the fact that house prices have come down substantially from their peaks really helped to drive affordability for instance, a national house price indices with a pickup we've seen this past year they are mostly down about 20-25% from where they had been at the peak of the house prices in 2006. so between mortgage rates at a 65 your low and house prices down substantially from their peak, that's driven

9:22 am

affordability to it very high levels. and that helps to encourage turnaround in housing demand, home sales and so when. there are still some very hard headwinds. marty mentioned them, relatively high rate of unemployment. we've had high unemployment for long periods time. that's a powerful headwinds pushing back on housing demand. unemployed people no longer biomes. the market has changed a bit over the last few years. but even with that headwind have seen a pickup in home sales. home sales were up about 9% over in 2012 compared to 2011. and we're expecting another eight to 10% increase in home sales in 2013 compared to the level in 2012. and i shows the level of home sales both for the existing home

9:23 am

sales market in lieu, and for the new home market in green. that is newly built homes in green. you can see even with the increase in home sales we had in 2012, and the projected increase in home sales in 2013, while we're moving in the right trajectory, home sales are still much, much less than what they were at any time, you know, from 2000-2007. so we are moving in the right direction to affordability is very high. that's helping turnabout housing demand, promote home sales, but even with the pickup in home sales at sales are still at a relatively low level compared to where they had been. i want to talk a little bit about house prices, and i'd like to think in terms of the forces that affect house prices by looking at the excess supply of vacant homes on the marketplace. and what i plotted here is in metric we put together that measures the excess above normal

9:24 am

supply of they can housing across the u.s. we look at both rental market as well as a single-family for sale market. and we had a large oversupply of vacant housing in the u.s. at the peak of the housing side. we had about 2 million, at least 2 million excess above normal they could housing units in the marketplace. and whenever there's a large excess supply in the marketplace, the force is for prices to come down, randy to come down in the rental market. indeed, that's what we saw after 2006, a lot of downward pressure of pricing, even rent in the rental market. let's take a look what happened over the last three years. we have worked off a lot of that excess they can supply. in large part because construction levels have been depressed.

9:25 am

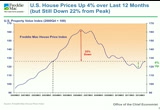

we continue to have households, not as robust as they were maybe five or 10 years ago but we have had household formation over the last year there've been on net 1 million new households formed in the u.s., but we only completed about six or thousand new housing development. so that difference between what's new housing constructed and the total amount of net new houses formation helps absorb the vacant oversupply of housing that we see in the u.s. and so we have returned to almost a good balance between the overall supply and demand of housing in the u.s., it has helped to encourage a tournament in house prices. this is a thought that national house price index that we created, freddie mac, and you can see the big run up in house prices in 2006 and the big crash there have to. house prices over the last year by this metric are up 4%. that's the best news we've had

9:26 am

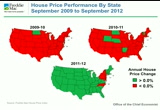

and house price in years, even with a 4% increase in national house price index we still have house prices down about 22% from their peak levels. i do anticipate further increases in 2013 the again, we are expecting about another three to 4% increase in national house price indices during the course of the coming year. was especially different over the past year is not just that national house price indices are starting to turn up, but the increase in home values have been very broad-based geographically across the u.s. and just to give you a real simple snapshot on that, take a look at the last three years in terms of the states that have seen increases in house prices and states that are in green are states that have had a house price gains over the past year. we can see 2009-'10, 2010-11, 2011-12. the last year has been remarkably different from the prior year's because the house

9:27 am

price improvement has been very broad-based geographically notches in the national index but throughout much of the country. if we look at the rental market what we've seen is a decline in rental vacancy rates which is a blue bars in outside over the last three years. rental vacancy rates across the u.s. are down about 2.5 percentage points where they had been three years ago. and with the declines in vacancy rates in the rental market, we have begun to see a turnaround in level of rent. rant is up over the last two, three years. national indices as well as many local markets around the country. and, in fact, just like in a single farmer for sale market, the decline in vacancy rates in the rental market again, very broad-based geographically. those markets especially that have been very hard hit by the housing downturn such as

9:28 am

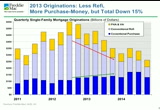

florida, arizona, new mexico, california and so on, those are some the markets where we have seen the largest declines in vacancy rates in rental apartments over the last three years. i want to turn up and close with some comments about the mortgage market. so mortgage origination on the single-family properties for 2012 came in i think somewhere around $2 trillion. that's her estimate, about $2 trillion of originations with about 75-80% of the volume for refinance. our expectation is that for 2013 we're going to see an increase in purchase money originations, about a 10% increase in purchase money originations, but also we're going to see a decline in the refinance origination. i'll tell you why. many borrowers have already refinanced over the last year, 18 months. they have locked in low interest rates of a very unlikely to come back into the market to

9:29 am

refinance right now. furthermore, while we have the lowest mortgage rates and 65 years and would have been for a while now, i do think obese and gradual upward pressure mortgage rates over 2013 but i still expect 30 year fixed rates as you're about 3% today, to remain below 4% in 2013 them but they will be higher later in the event are now. divided into 2013 will begin approaching about 4% of a 30 year fixed-rate mortgage rates. that's going to choke off some of the incentive to revive. so while we have purchased many origination rising, we have refinance originations are now forecast coming down, and since that such a big part of the market today, that's sufficient to actually reduce the total level of single-family origination because we have been coming down about 50% 2013 compared to 2012, not because of purchase money, but because of less refinance. less refinance but refinance will still be the bulk of lending in the single-family

9:30 am

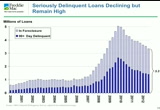

market in 2013. turning to the multifamily originations, these -- we saw a big pickup over the last couple of years, in large part because apartment owners are taking advantage of low interest rates and refinancing a debt they have on their buildings. they're expecting about 5% increase in multifamily originations in 2013 compared to 2012 come in part because there's been an increase in construction and transactions and multifamily apartment buildings, but also because they will be continuation of refinance activity. and then finally, i just want to close with the comment about the series leader link below to what i think as a proxy for the shadow inventory in the marketplace that we hear so much about. we have a large number of single families in the u.s. that are seriously delinquent, that is 90

9:31 am

days delinquent or in foreclosure proceedings. that has come down a lot. we had about 5 million single-family homes that had loans that were seriously delinquent three years ago. that has come down to about 3 million today. still, that's very high number, that's about triple what would we think of as an average, about triple what we saw 10, 15 years ago. in a single family markets are still at large stock of troubled loans we have. the industry as a whole has been working that down. still relatively high, and we'll continue to see properties come through the foreclosure proceedings cycle and come out as real estate owned and as aria sales in the single-family market over the course of the next year. what is so different in workplace today is that we have much stronger housing demand because affordability is so

9:32 am

strong in many home buyers looking to buy homes here so even as we continue to see some flow coming out in terms of reo sales in the marketplace, the increased demand for homes will still help to absorb fat, and provide room for increases in home values in the coming year. so thanks again to the chamber and the foundation for the opportunity to share our views, and i will turn it back to marty. >> thank you very much, frank. we will have john felmy from api next. >> thank you much for inviting me, marty. and thank you all for coming. we are just a couple degrees of getting to be just a which is traditional for the washington, d.c. area on presidents' day. i've lived here for 35 years and we had about 10 big snowfalls this time of year so we just dodged it is cheaper also want to thank you for coming out and hearing economists, since to

9:33 am

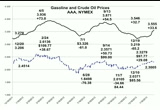

folks to take the opportunity will tell you a bad economist jeffrey what's the definition of an economist? as many of course but my favorite one is an economist is what is real good with numbers but doesn't have the personality to be an accountant. [laughter] so i'm going to do is go through, what's going on in the oil and gas industry, what the opportunities are and what we can do in terms of working in an important aspect of it come. the oil and gas industry of course is large. it's an important quantity of the economy. and so you have to pay attention to those facts in terms of how the overall economic situation is. so if we start first, this is what educational effort and so if you're getting credit for this, this is what's going on with gasoline and crude oil price. the top one is the retail price of gasoline according to aaa, the bottom line is the price of west texas intermediate from nynex in dollars per gallon.

9:34 am

if you just like per barrel cost it's hard to compare the two but if you just convert them in terms of dollars per gallon you can see how the two values move together. we have seen gasoline prices that recently over 30 cents account and using crude prices up by almost 30 cents a gallon. so there's no mystery in terms of what's happening between crude oil and taxes can you talk about 80% of the cost of gasoline and so when. and so what you need to do is just divide by 42 and that will tell you pretty much what's going on in terms of these markets. you can't have -- you can have other factors that can affect those margins, but that gap between the crude oil price and the retail gasoline price, the biggest chunk of that is taxes, roughly about 50 cents a gallon, federal and state. every thing else is defining, transporting and delivering a. i put this chart up because it also has an impact on the u.s. economy. the average household probably spends about $2700 on gasoline.

9:35 am

we use about 130 billion gallons of gasoline a year. so for every penny increase in the cost of gasoline, that's 1.3 billion that it spent more on gasoline instead of other goods and services. so there's clearly an impact one has to pay attention to on the. we've seen this over and over but if you look back over the last 40 years or so, that difference between crude oil prices and gasoline prices is averaged about a dollar something as i said, brother of that is 50 cents in tax but it concluded have an impact in terms of consumer spending and so when. let's see if i can get this to work at one of the big things that are also here is well, you know, gasoline prices go up like a rocket and come down like a feather. that's what everybody a search but it's not always true. so i look at the last two price increases we had over the last year, and you see that the jagged line is a refill price

9:36 am

and the other defines kind of symmetry actions of how fast they go up and how fast they come down. this was earlier in 2012 and you can see it's almost vertically symmetric. so when you hear those arguments, don't take them out so that face valley. the second half-year we saw another price increase. again, same case. i would be very careful about it. but irrespective of the, why are crude prices up so much was i like to say it's three defected. china, china, china but if what we've seen is record demand for oil worldwide, even though the u.s. is still a large player but much smaller than it used to be and as long as we continue to growth in demand in places like china, buying what, 24 million cars, growth rates of 7.5% followed by india, you see a powerful movement forward in terms of demand. and so with tight supplies, for chile we're seeing some positive aspects in u.s. and other parts around the globe so we haven't seen the real spikes. what you do see is a case of

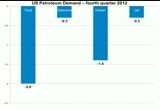

9:37 am

relatively tight market. the u.s. demand is down, and this is reflected in. what you seems to demand is down, gasoline demand is down which is tied more to things that retail sales, employment and so on. diesel demand is also down and that's tied more to the production side of the economy, whether its production of exports and when. and i carefully compare these diesel demand numbers with bob's numbers because they should move together. if they don't one of us has a problem, but they pretty much followed each other. we've seen these of demand. jet fuel has been down for 2012 and a lot of that is packing place for them having more efficient fuel, more efficient aircraft and so on. but if i turn to the fourth quarter we can see that things are still down. in particular the diesel demand was down. when i heard that gdp was down, it didn't surprise me too much because that's so tightly controlled or tied into the

9:38 am

composer of the economy and so on. again we saw about decline in total overall petrone, total gasoline to me. the good news from this chart is that if you look forward in the january numbers we have some prevented data on it, both for apis weekly statistics and energy information administration's, we saw diesel demand down but we did see gasoline demand up. that's a positive sign but hopefully we'll see this continue. but i will agree after will delete week economy as reflected through the lens of the fuel demand. what else is going on? natural gas. if you look at the top line, that is the price of crude oil in dollars per million btu but the bottom line is the price of natural gas. you can see how much cheaper natural gas has become. it's one-fifth in some cases of what the per cost isn't so. why? because we have all these developers of shale gas around the country. we've got of course the big shale gas play in the pennsylvania area, my home

9:39 am

state, marsalis, which also got oil in north dakota, south dakota and solar. that's led to increase in production of both oil and natural gas, which is, ma five years ago we would have been able to insist that that. that's good news in terms of supply. it's good news in terms of energy costs. it's good news in terms of employment. one of the previous slides that was up that showed in 2009-10, joe sebok apposite increases was north dakota. that's not the price given what's happened that north dakota is now the second largest egg producer of oil in the country. why? we have the technology. those of you who remember the 6 million dollar man, lee majors, it's because we've had dramatic improvements in the technology and hydraulic brockton, horizontally but we've also had improvement in deepwater drilling and canadian oil sands development. so we've seen this technological improvements that have really dramatically changed the course

9:40 am

of production that we would've never dreamed of. so what i'm going to close with is that we have an opportunity based on an ihs study to generate millions of jobs, trillions of investment, and billions if not trillions of federal, state and local revenues. we have the opportunity to do this just for nonconventional oil alone. so basically what we have right now is a choice. we can either make wise decisions moving over to develop, indeed all of the above resources, including oil, gas, coal, nuclear, renewables and so on, or we can repeat some mistakes of the past. in particular some of the proposals for taxing the oil and gas industry are repeated mistakes of the past. and we have potential for more regulation which could slow down the whole process. and, finally, if we don't get access to resources in this country, we won't be able to develop those oil and gas resources. so we have an opportunity

9:41 am

once-in-a-lifetime, you know, in terms i've been analyzing energy for about 40 years. this is the first time i can say that we really can move forward so that between what we produce in this country, between imports from canada and biofuels, we can become energy self-sufficient from a north american basis. and i would've never dreamed that was possible only five years ago. something so much for your time, and i will turn it over to the next speaker. >> thank you. [applause] spent we will have bob costello now. >> good morning. thank you, marty. thank you, al, for having me. so i represent the trucking industry, and i think it is a sort of a unique view, a different sort of you do -- viewpoint. the reason is it is a $600 billion industry, and it halt 67% of all the freight in the u.s. so it gives us a very unique insight into what i call a good portion of economy.

9:42 am

we don't put services on the back of traders. but we put almost everything else, anything you can touch and feel. and so i like a lot of people like to look at this and see what it is showing us. as john said, this year, let me say with this is. eucalyptus volumes of trucking in a couple of different ways. one is the amount of weight that is moved and that's what john referred to, the tonnage. another one is number of shipments are we call it loads. they measure two different things. for a lot of freight, most typical box traders you see. often is completely full, you can put any more freight onto hd by your well below the federal weight limits. so doesn't always match out, tonnage has always match of the overall it was up 2.4% but in the fourth quarter it was off 1% from a year earlier. even if you look at the number of loads, that was only up 8%

9:43 am

lash and it was a 2.1% from year earlier. i'm going to show you why the difference is, because it gives us insight as to what's going in the economy. like a lot of industries, small firms in the trucking industry are having a particularly hard time. they are having a difficult time reinvesting the capital, turning over the trucks. i will tell you that in a minute. and their bond as a result are bound even more than larger carriers. like a lot of parts o of the economy, small businesses are having a difficult time. all right. this shows different sectors and it gives us insight into what is going in the economy and what's not. that's a typical boxster. nothing special about it. doesn't have a refrigeration on it. it's not a tank truck. it's not flatbed. and that you can see was off and off significantly last year. especially forthwith.

9:44 am

energy production of the law. you use sand, water, and a little bit of chemicals. all that, it all goes into trucks and it is all very heady freight. that's why tonnage overall is going better than the number of loads. that freight when you measure the weight counts were. very heady freight, that's flat bed. so again, temperature controlled is mainly food. although it's interesting, a lot more electronics are going in temperature controlled eric not have your degree but they don't want to get very hot or very cold. but most of temperature controlled is food. so anyway, this is interesting because it just confirms what we already know, we're producing more energy and housing starting to rebound.

9:45 am

in this industry is than it was a few years ago. economy essentially rebound. it's not growing as fast as it should as marty shoji, but it has rebounded. but prior to the recession, we are not operating as many trucks as we once did your. ..

9:46 am

and demand demand being the red line, the number of shipments and the blue line being the number of trucks we are operating, you can see when you got into the recession of course we had too much equipment on our hands. oversupplies and the price plummeted. but what happened? we started to see a rebound in demand and we kept cutting the fleet and now they are matched up. a lot of our transports are similar whether it is the airlines or trucking companies but are they trying to do? they try to get the capacity to reach the amount of demand it's

9:47 am

not just buying a bunch of sharks in anticipation of the recovery which is very unique and. we have matured as an industry. i said earlier we need to invest significantly in new equipment. this shows you that. it is mainly that large tractor-trailer combination uzi on the highway in the five and have your area would be historically the normal. we were approaching seven years and came down in 2012 a little bit but you are still six and a half years. to get that age down to where it's been in about five and a half years it would take an

9:48 am

investment of at least $40 billion. so it's very reflective of a lot of the industries and economy and those investments in the down time are nervous about the uncertainty and policy you don't want to hire to many people and invest in too many capital we have a lot of hard testing that needs to take place once the economy starts to do better. the last couple slices on labor. despite elevated on employment rates and so forth, we actually have a labor issue. lots of jobs in trucking. one way we know that this is going on besides talking to a lot of fleet's is we look at the driver turnover rates. if they are in very high demand, i call them the free agents of trucking. they can go to any -- if you are a good driver with a good safety record and so forth, you can go

9:49 am

to any company you want and they will give you a sign on bonus. a lot of companies give a sign on bonus just to come to them and start driving. uzi the driver turnover rate is increasing and we bottomed out at 50 percent. i know that seems high but that's probably about the floor for this industry. even in those times when we are calling less freight you can go to different companies. so it is the back up to 100% turnover rate with a lot of pressure in the driver market and in fact we have the trucking each year. i grew up in a town of 100,000 that astounds me. there's many reasons we need that many drivers. we will start growing the fleet more. you have to had a driver. no driverless truck said this

9:50 am

point. our drivers or older on average than most employees out there it is the number one reason. we had a shortage of drivers about 20, 25,000. because housing started to improve about 25% last year, the construction employment was up about 1% so if they start hiring more people because of the continued growth in the construction industry that is going to put even more pressure on our industry we could be short at the of the words the to end of the year months we have an industry that wants to hire a lot of people and you have to be on the road -- today it is about a week at a time before you get home. there are certain parts of the industry is longer than that for most drivers. so the economy has slowed, you

9:51 am

know, we talked to the trucking companies that say the freight is a little better this year but i feel a lot of a stalking happened in the supply chain in the fourth quarter since probably significantly early on. we need to invest in all of capital in the airports of the $40 billion for the good trailers and others, and of course we have an industry that is looking to hire in this economy. that's all i have. >> thank you very much, bob. [applause] now we get to the fun part of the programs we are going to open up for questions in just a minute. if any of you have any questions, write them down. there will be microphones circulating. address them to whoever on the panel you want to and those on the panel can jump in and give their two cents' worth.

9:52 am

it's not a deal where we give one question or one interviewed before we get to that i want to ask some questions and the first one is also to bob and john as well and that is what are we seeing in terms of the lending availability? in the housing market specifically we see great rates and high affordability. are the banks starting to lend again? is there an availability of credit and the same in the trucking area. they are not precious with cash for the most part. what do the financing options look like? in terms of the commercial loans, the companies generally don't use bank as a primary source but what is the availability of the credit for them to expand into this growing energy supply? how quickly can we get in and start to take advantage of this? we will start with frank and

9:53 am

moved across. what is the bank lending situation or the availability of the credit situation in your industry? >> it's gotten better. we have about $2 trillion in the senior family origination and 2012. that is the biggest that we have had about three or four years in a single-family space and there are certain products that are not available that have been available at the peak of the program but those are the high risk products that disappeared from the market so you don't see the sisters, nina and sissa, nina de no dak loans. fairly common and 06 and the beginning of 07. those bills have gone away but what we see now are fully documented loans, fully documented underwriting and the

9:54 am

fixed rate 90 to 95% of all of the loans originated or the long-term fixed-rate mortgages. i think lenders have been a bit more cautious in recent years. in 2006 and 2007 what happens in terms of the regulation in the qualified mortgages and residential mortgages and once the rules come out it provides more certainty for the lenders so they can decide what's the right perimeter they want to underwrite going forward. we have seen better availability on the commercial real-estate side compared to the single-family side. so on the commercial side, we began to see listening of the credit underwriting standards.

9:55 am

>> very good. in terms of tracking the companies, it has gotten better as well, but i would say that it's still a challenge for my industry. one of the biggest challenges we tavis our equipment costs have surged over the past few years believe it or not even in the deficit of the recession and the reason is we actually had it epa mandated insurance, we had the fuel change and then we had the epa mandated engines that changed from 06 to today and what that did to the cost is a typical we call with a tractor the truck that hauls the tractor-trailer and 06 would cost about $95,000 to get that type of vehicle today it is $125,000 as we have added so much more equipment for the environment. the good news is it is much better for the environment. but there has been a cost associated with that.

9:56 am

so, costs are up and the lending is not what it once was. so we have many -- i showed you the small fleets are not growing the number of trucks they operate. in part the reason they are doing that, and i also showed you the age has gone up significantly so they are not worth as much as a 3-year-old truck, so we have many small fleets having to sell used trucks to afford one new one. part of that is because they cannot get financing for as much so they have to put more down. the of a thing on this that i have seen over the last two years is lease financing used to be 10%. any trucks that you would acquire in a year especially the smaller fleets would be maybe 10% of the trucks would be from the finance leasing and the rest of the purchases. today is 30 to 40% because it is the only way that they can get

9:57 am

it. they can't get all of the financing that they need for the purchasers comes of they are turning more to the leasing. it is a challenge and one that is holding us back a little bit. >> i would have to agree with that. there are thousands of small wheel and gas companies that rely on financing for moving forward for the investments they make and things are improving but there are a couple complicated things that are kind of interesting. one is dodd-frank the potential regulations in terms of how you classify certain contracts whether they are traded on exchanges versus bilateral deals where you get financing based on the ultimate outcome of your production, and those things we are still working our way through so they could be problematic. the other thing that is interesting in the industry that is a challenge has to do with housing. for some of the areas where you have seen like north dakota, a lot of workers move there and the need housing. unfortunately in terms of getting a mortgage, there are

9:58 am

some rules that can prevent you from getting a mortgage if you haven't worked at a job for a certain period, so for the areas that has been a limitation in terms of labor and i was talking to a banker in north dakota. if there was a wave you could deal with that you would get a lot more housing and workers and production. >> i'm going to start with you and the others can cheyenne, too the industry and the potential for the growth in that industry driving growth in the u.s.. how fast -- and you talked about some of the obstacles but held fast can the energy be exploited and how fast can a show improvement in the general economy? you are not going to go from finding this stuff on the ground to pumping it in the tank in six

9:59 am

months. but you would start to see i think fairly noticeable and preference in the u.s. economy if we were to exploit these natural resources to a much greater extent so how fast can we do them and what do you see as the obstacles cracks >> one of the biggest is getting access to the resources. we have a vast amount of oil and gas in the country that off-limits to the east coast, west coast, alaska. until you open the areas to be able to start the whole process, nothing can happen so we need to move forward on the five-year plan for the areas that have been delayed. we need to carefully look at some of the restrictions that we have seen over the past four years so once that happens you can start a schedule of the environmental assessments you have to do and then you start

10:00 am

leasing and then you have exploration activities so it can be a couple years before you start drilling so the key thing we need to do is move forward as quickly as possible let's open these areas and go to the process that has to be done because then you can start getting the lease revenue coming into the government you get royalties from production and everything else that falls along in terms of the investments and jobs and so on so the big aspect is access but if we have regulatory policies to come into place that slow them down then it's even more of a challenge. >> where do you get the trucks to facilitate this kind of growth? you pointed out the flatbeds,

10:01 am

the trucks were extractions related and there is a shortage and i guess you can't just take any truck and turn it into a flat bed or tanker can you? >> you can do certain extent. i have a large number that has taken 500 of his trucks where should the freight was down and he moved it over the sector to help with a natural gas at the north dakota and sorts. actually the challenge is getting all the tankers that are needed. the manufacturers cannot build them fast enough. the interesting thing on the energy side i might add there's a lot of interest as you might imagine by the trucking companies to get natural gas trucks, not the local delivery trucks that you see but the big heavy-duty trucks and you have the fuel that costs half on the

10:02 am

per gallon basis so there is a lot of interest and i get a lot of questions about that but there's obstacles. bonn is today the trucks cost 50 to $60,000 more than a diesel so you add that to the 125 fight told you earlier and then you get your maintenance facilities and so forth. but there is a lot of interest in the industry for a small portion of the heavy-duty and fueling that is another issue on the trucks to natural gas. >> we've heard about the holes in shortages and rental shortages and the like in some of these parts of the u.s. where we are starting to see the energy pickup. you don't 58 gove with a light switch to law starting to meet that demand and see those areas with rising housing prices, are

10:03 am

we seeing more construction in those areas? are there shortages that are specific to those areas and things we should be doing in anticipation of more growth in these areas? >> we have seen a pickup in those markets. john mentioned north dakota as an example and they have one of the strongest housing markets for years already the turnaround in the demand wasn't just in the last six to 12 months in north dakota. it's been the strongest for years. if you look at home values they were up sharply already three years ago in north dakota reflecting the demand for housing and builders have responded to building a fair amount of rental and north dakota as well so there is an increase in the new construction on a percentage basis anne

10:04 am

gurley the strongest increase we've seen in the new starts compared to other states in the last three years. >> we received a little bit of black when the chamber started to focus on the area and people focused on a very narrowly as the gas production but in effect housing demand and supply, trucking and many small businesses and it affects not just the fund mental and put but there's a lot of other pieces that drive growth and gdp growth and job growth if we would pull some and get a better mix of regulations can really start to exploit some of these resources that we have cash. next question and then i'm going to turn it over to you out there. the q4 versus what we are seeing

10:05 am

-- we've seen an economy that's been going pretty consistently, but in a pretty -- for three and a half years. there's been a couple of good quarters and a couple of bad quarters. the fourth quarter was one of those bad quarters from a top line number. i recruited a little bit in my presentation because i think we need to start to peel the onion down a little bit. you see the consumption growth was much stronger in the fourth quarter than in the third quarter. it was federal spending pretty much defense spending. how do you look at that fourth quarter compared to the first half of this year? is the harbinger of things to come or is it going to look like an aberration in their rearview mirror i will start with frank and then move this way. >> was a bit of an aberration and one of the positives i saw in the fourth quarter was the contribution on the housing sector and that is the residential investment.

10:06 am

to become. for much of the recovery the housing hasn't been there. housing continues to weaken and be a subtraction for economic activity in 2009, 2010, 2011. finally in 2012 housing began to contribute and takes up in the housing starts and flows through the residential investment and the investment contributed about four tenths of a percentage point in the overall gdp or helped make it less negative. of what we are expecting to see is a bigger role for housing in supporting economic growth in 2013 to the we are expecting that over 2013 housing in the residential investment will contribute close to half a percentage point of overall gdp growth. >> i'm in the same boat i'm not overly concerned about the

10:07 am

trading. last spring i was starting to get concerned about inventory levels and the supply chain and something we were hearing from our members, their customers and those showing up in the inventory to sales ratios so, a big chunk of that was to change the d stocking a few well throughout the supply chain saw you saw that the numbers were off on bud year-over-year period in the fourth quarter and even more so than the gdp reading. i look at this as a positive and if we get the inventories back to where they need to be that will help the volumes this year so not overly concerned, and again, we did like to see the business investment and household consumption pickup. islamic is a continuation of you

10:08 am

see in the recovery. the beginning of the recovery what we saw was the weak gasoline demand and that is driven by employment and sales and so on and that's consistent but for much of the recovery come to that fairly strong diesel demand in the that is consistent with a lot of the data but then you started to see the shift through last year, 2012, ultimately ending as i said with low were diesel demand and the fourth quarter relative to gasoline. as i mentioned going forward we have seen a continuation of the low diesel demand from the preliminary data for january but we have seen a rebound in gasoline which is consistent with some of the sales data and so on so it seems like the ship is turning a little bit. >> now we are going to open up so if you have a question put up your hand and we will bring in microphone around and i identify yourself and direct a question to anyone here and we will see what we can do with it. do we have any takers?

10:09 am

>> good morning. exxonmobil. my question is for you what. sometime in the next few months to the point of your remarks we are to be faced with sequestration we are in the beginning of some kind of a reduction in government spending. can you give your sense of how you think that might play out and what the implications would be for the economy? and given the fact that consumer spending would is still probably about 70% of the gdp what the implications for the consumer? roi >> i think the sequestration the worst aspect of the sequestration is not the overall cut because we know we need to trim spending and change the trajectory going forward ahead. predominantly entitlement.

10:10 am

without that i don't think we will get the budget under control and some point we will be downgraded by the other agencies and of some point we will start to see interest rate increases that the people that hold their debt to around the world less interested in holding it with very low interest rates. all of those will affect the u.s. economy. so that having been said when i look at the sequestration i don't look at the cuts as really impacting the economy in a negative way. they are not keen to help growth in the short term, but they have offsetting factors which mitigate the negative. the problem with sequestration is the way the cuts will take place because what we tell the congressman and the senators that's why we send them here we send them to spend money. that's absolutely what we do because we expect them to provide public goods, infrastructure, education,

10:11 am

national defense so we send them here to spend and we know in order to pay for those goods we have to what tax so that they are year to do is to spend and attack what we hope they do is prioritize. we hope they look at what is out there and see what do i need to do first, how much do i need to do and only do that and sequestration with flies in the face of the reason for sending them here. it obviates the need in the legislates against the prioritization. we tell them go out and locked everything the same. anybody that's coming budget whether it is divisional budget, department budget, company budget knows the ball game and we have a little bit here in little let there and we put a project in that maybe we don't need and we know that if we get cut we are going to cut that one

10:12 am

first what. with this at is we can do that. go and function across and just take off what would. that is stupid policy. what we ought to do is find a way to prioritize these cuts. think about it. that was the job of the super committee. there was an agreement made a couple years coming year and a half or so ago that you would get a debt ceiling increase and there would be 1.2 trillion in cuts and get the second increase for another to the super committee was to put together and they were supposed to prioritize. they were select members of a congress that were supposed to prioritize and a dandridge. kind of knowing they might not do it the congress said we are going to put something that is so draconian and stupid that nobody would let it happen and low and behold that is what we are dealing with. that is a sad state of affairs from the political process it's

10:13 am

a very sad state of affairs. so now to come back and say what we should do with the sequestration, i find it amazing the president who talks so much about balance and fairness, a year ago balance on getting the budget under control was four for 01 in spending for every dollar in tax increases and then as we went along we salles the discussion shifted and the prospects rose and fell the balance became 2 for 1. then in december after, the talk was kind of 1-1 and then there was zero was spending a cuts to the tax increase and now we are actually hearing negative. it's not 2-1. the president wants to cut those the were already made in the future and he wants to replace the agreement which was then you would do this to bed

10:14 am

sequestration policy of congress couldn't come up with a prioritized cut and we are going to replace those with more tax increases and by the way, john, thanks for stepping up. >> okay because they are all aimed only oil and gas extraction industries and things like that. so, this isn't a good policy. what we would like to see is some prioritization. should we do away with the kutz? that isn't a good thing either because when you look down the road we have not established a sustainable fiscal policy. we have a policy that under the forecast starts to turn up and the debt to gdp ratio starts to rise and by the way if you look at the interest-rate assumptions underlining those, they are pretty pollyanna. even beyond that, very, very

10:15 am

modest increases in interest rates. think about it with $16 trillion in debt, every percentage point increase in the interest rate is about 160 billion to the debt service and that very quickly starts to cause an increasing spiral. i worked a couple millennia ago we used to worry about the debt and deficit to gdp ratio of the 5.5 to 6% because that was the range which they could start to spiral out of control. we haven't seen anything remotely close to the deficit to gdp ratio of 6% in the last four years. by the way, even under the best assumptions we are looking at another two to three years before we get down to the 5% rate. so i think we need the kutz. eddy should be prioritized. those cuts across the border are

10:16 am

going to affect certain industries more than others. the defense industry is going to be impacted at more than others. we have to make a decision on how we want that to play out. you obviate the need for an across-the-board cut and there's not a good public policy. so i think the cuts are necessary. i don't think the cuts are so large that if they were instituted to come if the congress were to sit down and pick and prioritize the appropriate cut that they would lead to an economic downturn. when they were talking about the fiscal cliff they're going to lose $500 billion or more in the sequestration spending and increased taxes if you did nothing. and the $500 billion, 550 million-dollar total would cause a mild recession of something on the order of about half a percent of three tenths to five tenths% of gdp to look

10:17 am

at the forecast or cbo. so now we're talking about a sequestration is one-fifth of that and we've seen some tax increases the or possibly another fifth of that, so we were looking at something where we got 40% of that. i don't see a recession coming because of that and i think that there was and factored into that because in many cases, it reverts back to a very static approach. you do not look at what is happening in the housing which i think could be better than what many of us think. i don't think we are looking at the energy sector that has done tremendously well and could expand as well under the next as it did over the past and if we prioritized it would set the stage for doing even more of that on the road. >> i think in terms of energy you are right we have an

10:18 am

opportunity to move forward to generate jobs and energy security but it's going to take a conscientious decisions in terms of making decisions like, for example, the keystone exfil pipeline because you immediately start generating jobs and in all of the indirect effects. but unfortunately, what we have is a debate against it for some reason that somehow the opponent's think that stopping keystone xl will stop developing the oil sands, that is not true. they are worth something like ten times the gdp the notion they wouldn't be developed is silly so if you believe and environmentalism will bring it here because it is more the missions. we need to make decisions in terms of things like exports of energy. we have an opportunity with so much gas we are producing that we can export at a good price which keeps jobs in the country and so on so there are positive things we can do beyond the

10:19 am

budget process that will help the economy right now. >> other questions? >> we have one over here. >> the american public transportation association, you had some interesting facts on some of the subsets of the housing market. one might you have any observation on the new trends in housing perhaps try and caused by the board by generational changes or anything the housing market? was >> has the desire changed in some way with compared to the attitude several years ago? my take on the surveys over the

10:20 am

last few years is that desire for homeownership at some point in the lifecycle has not changed. families today are being formed and creating households. several of seem desirable for home ownership as younger cohorts. one thing that is different is a recognized of about to put my financial house in order first and save more money and there is recognition they are making a larger down payment. but i think that we will see over time they will have the same ultimate home ownership rate over their life cycle they may delay the time what they become a first-time homeowner.

10:21 am

over one's life cycle plus to 90% of households become a homeowner at some point in their life cycle that's a different number than i'm talking about. it's all households today that are renters the households of many different ages, young earth cohorts, old cohorts and 80 to 90% of all homeowners are at some point in their life cycle so that has not changed but the age at which people choose to become a first-time homebuyer in the transition to homeownership i think may have changed and i think that is probably going to be delayed relative to.

10:22 am

the rate of household growth will continue at about 1.2% per year. that is the production and we have about 120 million households in the u.s. if we do the math it works out to something new like 1.4 million new households per year. we had a pretty good year since last year and i think the trend is looking pretty good going forward which is good if you are a homebuilder and you've been able to survive the downturn so

10:23 am

far. >> in that formation and the net of the 40-year-old kids moving back with us. >> that is the take away and i don't know if i can convey that appropriately. >> that's right. they moved back into their parents' basement. >> other questions? >> when we look out there at these fiscal problems and the discussions, we have a state of the union coming at next week. what in your area would you wish for that what surprised you come and what do you expect? i will start with bob ho in the middle and we will work to the extremes. >> one of the things that we've been struggling with for a number of years and it's been a great partner with us and we are

10:24 am

not investing enough in our infrastructure. that's good government spending and creates a lot of jobs to increase its productivity in the long run and you have an industry here. how many industries do this? it's been saying for years please contact me more. we want the tax to go up. and so we would love to see some progress made on this. we've gotten so desperate in this area that we are not talking about perhaps the needs because politicians can't make a decision on this and haven't since the early nineties on a federal level maybe we need to go to the index. >> but you are talking about a fuel tax for the infrastructure and not to pay for subsidies, right? get one sold off against another and what we need is more infrastructure and that is a public good and that means to be paid for and generally with the

10:25 am

tax revenues. so i don't think anybody is faulting that. i think it is sold that we need more fuel tax and we can use that to reduce the deficit or pay for something else. the appeals tax was intended whether it's done successfully or not intended to pay for the infrastructure. >> absolutely, diversion. >> we are not happy about that. >> john, what are you hoping for? >> for some reason i haven't been consulted on that. the president in the campaign said he was four and all of the above energy policy so let's have some announcements that support that and move on these big decisions like keystone xl and leasing decisions, the five-year plan. really the things you need to do to be able to accomplish all of the above policy. i would say that we would also -- i would like to see us stop this discussion about taxing the industry and try to characterize

10:26 am

the subsidy which is simply not true and i would like to see more opportunities in terms of where can we open up areas that are off-limits right now because all of those combined can generate an enormous amount of opportunity for the economy right when we need it. >> frank? >> i will just mention a couple of things. one thing is i think the lenders have been concerned about the implementation of the new regulations that affect the housing market. to the extent we get more clarity and certainty for with the framework will be like going forward i think the lenders can take advantage of some of the flexibility once they know what the rules or in extending the credit. i think it is an important one and its financial literacy to reach out to the industry to try

10:27 am

to promote financial literacy and education. we have an educated group of young folks that understood the importance of having a financial house in order, the and importance of having a good credit history and understanding what this means to be smart about using credit whether it is in the mortgages are the consumer or even student loans. >> thank you. one last call for questions if there's any help there can we get a microphone over here? and we are on this on time. >> i represent a mobile technology, broadband providers and probably all of those in the trucking industry and oil and gas is using more in this operation. anything the panel can say generally on the continued growth in the mobile broadband and technology generally? >> certainly from a trucking perspective, yes. it's been absolutely critical to

10:28 am

the industry over the last decade or so. the days of the drivers going to the pay phones and calling in for the next load now it pops up and tells them exactly where to go and when to be there and so forth and there's a lot of the penetration probably isn't even all the way there yet in trucking and there's a lot of opportunities. that's something they are willing to invest because it impacts the bottom line. >> the ability to capture what's going on in terms to distribute that back to the central location for the analysis dealing with understanding what is going on is essential to moving forward to be able to develop our energy resources much more quickly and efficiently. >> when he mentioned the payphones i chuckled a little bit. do they still would assist?

10:29 am

>> this has been an interesting discussion because it is an economy that when you look at there is a whole list of positives in the housing and energy. what's happening in the energy area yet what is happening in europe and abroad then there's a list of negatives and virtually every one of the negatives is self-inflicted. we have the potential for this economy to break out of the doldrums, push it above the 2.3% and may be significantly above it, but i think that our policy options or what is holding us back. but i would like to hear and see in the state of the union is a plan for addressing the long-term deficit over a reasonable length of time, one that does recognize and specifically addresses what is going on on the spending side and tells us what they are

10:30 am

thinking specifically on the tax side so that there is some evaluation that can be made. i think that would go a long way towards stimulating a debate on entitlement reform and tax reform and the congress, and that i think would be a plus for the economy as well so it is not all bad news even though it is a lousy rainy day i want to thank all of you for coming and hope we can do this again in a couple of months. thank you very much. [applause] >> [inaudible conversations]

10:31 am

as the chamber of commerce meeting comes to a close it is available anytime on the web site, go to c-span.org and search the library. some news that moved before they got under way during the chamber of commerce meeting the associated press report in the u.s. trade deficit narrowed in december and the imports plummeted and total exports rose. a smaller trade gap means they unlikely performed in the three months of last year than first estimated last week. we are also learning secretary of state john kerry is meeting with canada's foreign minister and one of the subjects they are going to discuss the controversy will keystone pipeline delude bring the oil from canada to

10:32 am

texas over the transnational pipeline. that meeting is scheduled for 2 p.m. with a press briefing after words at 2:30. we plan to have that leader on the c-span networks. we have more live programming to tell you about on the program today. defense secretary leon panetta will be honored having observed a steady improvement in the opportunity and well-being of our citizens, i can report to you that the state is old but the union as good. >> once again, keeping with the time honored tradition i've come to report to you on the state of the union and i am pleased to report that america is much improved and there is good reason to believe that improvement will continue.

10:33 am

>> my duty tonight is to report on the state of the union. >> not the state of the government, but of our american community and to set forth our responsibilities in the words of our founders to form a more perfect union. the state of the union is strong. >> as we gather tonight, our nation is at war, our economy is in recession and the civilized world faces unprecedented dangers, yet the state of the union has never been stronger. >> it is because of our people that our future is hopeful an hour journey goes forward and the state of our union is strong

10:34 am

first lady helen taft on discussing politics. >> i always had the satisfaction of knowing almost as he about politics and intricacies of any situation. i think any woman can discuss with her husband topics of national interest. i became familiar with more than politics. it involved real statesmanship. to now the annual bank of america economic forecast discussion

10:35 am

from the commonwealth club of california. economic advisers to presidents george w. bush and president obama beebee did the future of the economy as well as health care, education and entitlement policies. you will hear from the former chair of the council of economic advisers, christina romer and the bush economic adviser keith hennessey. this event from san francisco is just over an hour. >> midafternoon and welcome to today's meeting of the commonwealth club of california. i am massey bambara, the president of bank of america, a member of the commonwealth club board of governors and george chair for today's program. we also welcome the listeners on the radio and television and invite everyone to visit us on the internet at commonwealthclub.org. today we are pleased to present the economic forecast named in honor of the club's late past president and longtime board member dr. walter holey who

10:36 am

served as the chief economist and vice president of the bank of america. today's program is sponsored by the memorial fund and bank of america. today's program will feature a distinguished speakers with distinctive viewpoints. dr. christina romer, professor of economics at the university california berkeley and former chair of president obama's council of economic advisers. and mr. keith and hennessey who teaches at the stanford university school of business at stanford law school and served as director of the national economic council under president george w. bush. keith hennessey served as both director of the national economic council as assistant to president bush for economic policy. as a director of the national economic council during the 2008 financial crisis, mr. hennessey was at the center of one of the most volatile times in american history. she was a senior white house economic adviser where he coordinated the design of the president's policies on taxes,

10:37 am

health care, pensions, energy and financial markets and institutions among others. mr. hennessey spent more than 15 years and economic policy rules for the senior elected officials. before his time in the white house, he worked on capitol hill for more than seven years as economics adviser to the former senate majority leader trent lott. since leaving the white house, mr. hennessey has been a television commentator and start a blog named one of top 25 economic blogs by the "wall street journal." he also served as a member of the financial crisis inquiry commission. mr. hennessey holds an undergraduate degree from stanford and master's degree in public policy from harvard university school of government. as the chair of president obama's council of economic advisers from january, 2009 until september, 2010, dr. christina romer was one of the four economic principles who met with president obama deily to design and guided the

10:38 am